Quick answer

You don’t need a category budget to make a spending decision. Start with cash you can actually use, subtract money that already has a job (bills, upcoming payments, protected savings), and the leftover is what’s genuinely available for today. That simple estimate, free from spreadsheets or guilt, gives you enough clarity to say “yes” or “not yet” to a purchase without overcomplicating your money.

A realistic money example

Imagine you have a checking balance of $2,400, but not all of it is free to spend right now. After subtracting what’s already committed, you see a clear daily number.

The $450 isn’t a rigid limit. It’s a signal that says, “this purchase probably fits today.” When you understand that number, you can buy a coffee, say yes to an unplanned dinner, or wait until payday without having to redo a budget.

How to estimate it

The idea is subtraction, not restriction. The formula works the same whether you do it on paper, in a notes app, or automatically with Pip:

Estimated spendable today = usable cash - near-term bills - protected savings - already-committed card/debit spending - other known obligations.

- Start with usable cash: your checking balance plus any savings set aside for everyday spending, not emergency funds or long-term goals.

- List near-term obligations, anything that will leave your account before your next income, like rent, car payments, minimum card payments, and subscriptions due soon.

- Set aside protected savings. Money you’ve mentally marked as “don’t touch,” like an emergency buffer, should come out of the picture.

- Account for already-committed spending. If you have a pending debit transaction or an automatic bill that will hit tomorrow, deduct it.

- Watch for timing gaps. A payment due in three days is urgent if your next deposit is in four. If you’re paid tomorrow, a rent payment due next week can wait.

No categories, no envelope system, no fixed spending cap. Just a realistic look at what’s actually free after commitments. Re-run the estimate whenever you’re unsure about a purchase or your account changes.

What can make this estimate wrong

Even a simple subtraction can get tripped up. Watch for:

- Pending transactions or holds. A restaurant may put a temporary hold that alters your available balance; that hold might not appear instantly.

- Forgotten obligations. A friend’s birthday dinner you promised to split, or a yearly subscription you forgot about, can be missed.

- Timing uncertainty. If you’re paid irregularly, it’s harder to predict when bills will withdraw and when income will land.

- Emergency spending. Unplanned costs like a car repair can upset the math immediately.

- Mental-accounting drift. Over time you might “borrow” from protected savings in your head, making the number less reliable.

When your estimate is stale or incomplete, the daily number can feel too generous or too tight. That’s why it’s best treated as a reality check, not a precise directive.

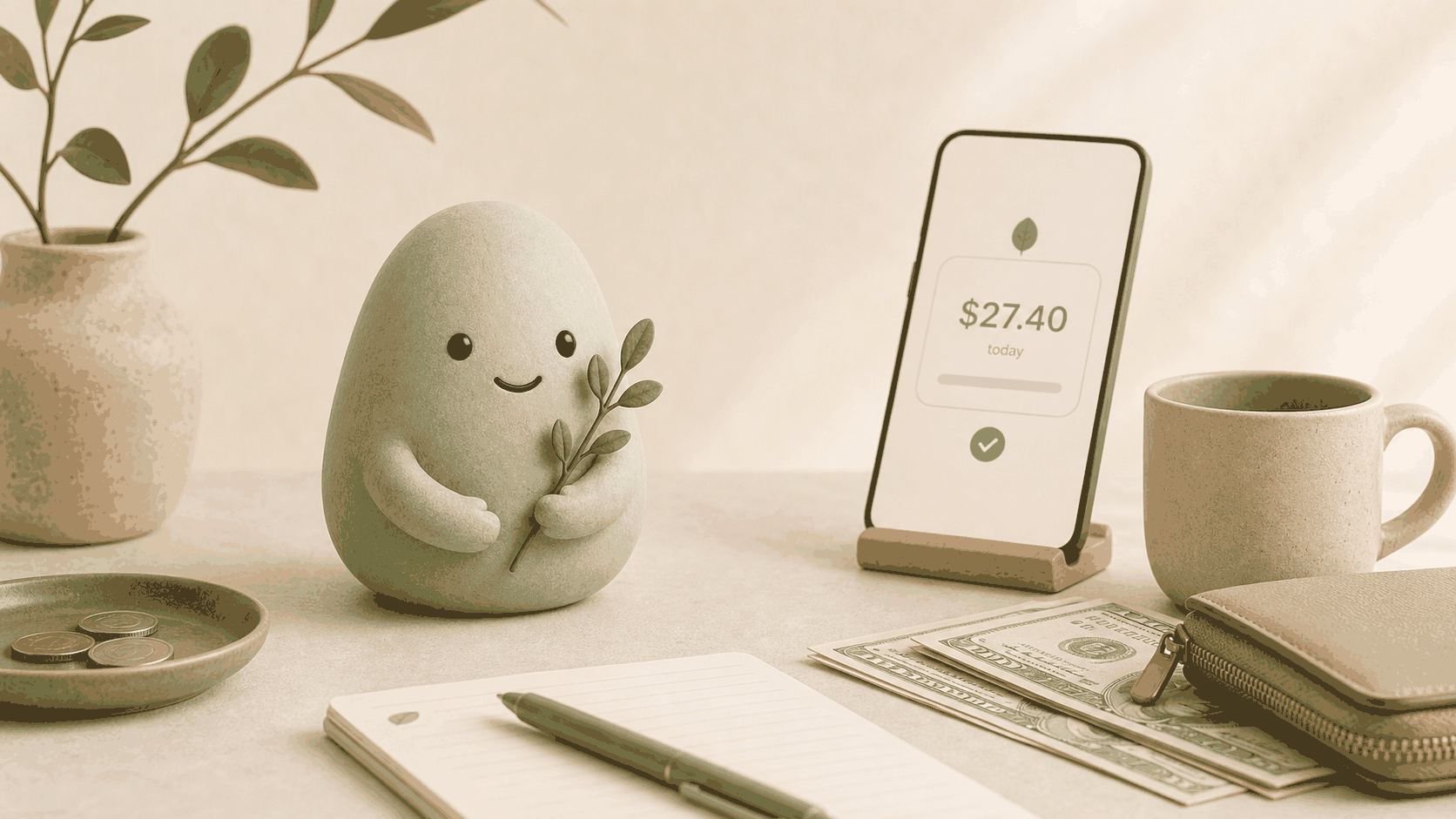

How Pip handles it

Pip does the same subtraction automatically, using a read-only connection to your linked checking and savings accounts. It pulls your current balances, identifies upcoming transactions, and calculates Spendable Cash Today, a single number you can glance at before you spend.

Because Pip does not move money, your cash stays exactly where it is. The app does not store bank usernames or passwords; it relies on secure, token-based connections that you control. Those safeguards keep your accounts private while giving you an honest daily signal.

When the number is comfortably above what you’d like to spend, that purchase likely fits. When it’s lower than expected, you get a gentle pause, not a warning. Either way, the insight is not financial advice. It’s decision support: a quiet nudge that helps you act in line with what’s actually in your accounts, not just what the bank balance suggests.

You can learn more about how the number is built on our How the number works page, or dig into the difference between your bank balance and a spendable number in our post Why your bank balance is misleading.

FAQ

Can I really stop budgeting and still spend responsibly?

Yes, many people handle everyday spending without categories. A quick, honest sense of what’s available after bills and priorities is enough. Checking one number before you buy keeps you aware of your real cash position without the heavy planning of a traditional budget.

What if my daily spending number is low?

A low Spendable Cash Today number is feedback, not failure. It means that after upcoming obligations, there isn’t much extra today. You might postpone a purchase, wait until after payday, or rethink whether you want it. The number simply shows what the math says; it doesn’t judge.

How is this different from a traditional budget?

A traditional budget assigns category limits in advance. This approach gives you a single, live number that reflects what’s truly available right now. Instead of tracking whether you exceeded your groceries or entertainment bucket, you check if today’s purchase fits the overall picture.

Is my bank information safe if I check my number with Pip?

Pip uses a read-only connection, so the app can see balances and transactions but can never move money. It does not store bank usernames or passwords. Authentication is handled through industry-standard providers that you manage from your financial institution. For more details, visit our Security page.

Source notes

Pip uses a read-only account connection, does not move money, does not store bank usernames or passwords, and is not financial advice. This article reflects common cash-flow practices and the logic behind Pip’s Spendable Cash Today calculation. No external financial advice sources are cited, because Pip is not financial advice. Always verify your own account details for the most accurate picture.