Quick answer

Budget apps that require categories often fail people who hate organizing every expense. Pip replaces categories with a single daily number: Spendable Cash Today. By subtracting upcoming bills, card payments, and protected savings from your usable cash, it shows what’s available for today. No categories, no spreadsheets, no guilt. It’s a quick signal you can check in seconds. Pip is a budget app for people who hate categories, built around one low-pressure number. Here’s how it works.

How to estimate it

Pip’s formula is simple. You start with the usable cash across your checking and spendable accounts. From that, subtract near-term bills that must be paid before your next income (rent, utilities, credit card minimums, loan payments). Subtract any protected savings you’ve set aside for emergencies or goals. Finally, subtract already-committed card or debit spending that hasn’t yet cleared. The equation is:

Estimated spendable today = usable cash – near-term bills – protected savings – already-committed card/debit spending – other known obligations.

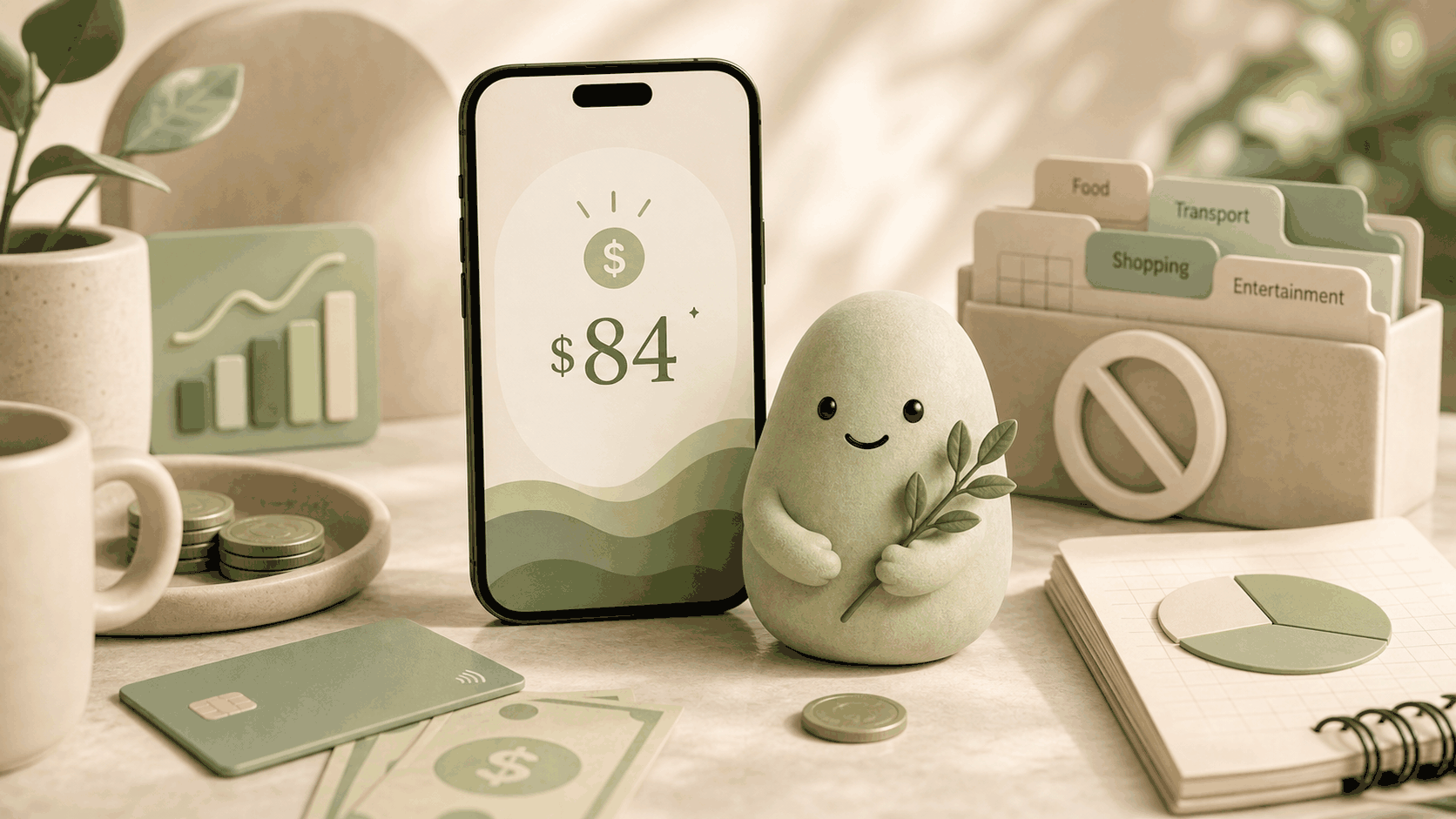

Here’s what that looks like with real numbers:

That result is your Spendable Cash Today. Traditional budgeting would then split that $600 into grocery, dining, entertainment, and a dozen other categories. Pip skips that fragmentation completely. Instead of forcing you to allocate every dollar into separate buckets, Pip gives you one trustworthy number. You don’t need to label a coffee run, a lunch out, or a spontaneous book purchase to stay aware. You just check the number before you spend.

Limits

Pip’s estimate depends on accurate, up-to-date account data. If a connected account is missing, or transactions haven’t posted yet (like a weekend check), your Spendable Cash Today might look higher than it actually is. Unexpected bills, forgotten subscriptions, or refunds still processing can also shift what’s truly available. Missing accounts, stale connections, and manual bill updates can further distort the number. If you haven’t added a recurring obligation yet, Pip can’t subtract it. Refunds that hit your account later than expected may temporarily inflate the number, and pending debit transactions may not be reflected until they settle. We can’t predict every cash need, like medical copays, car repairs, or last-minute gifts, so your daily number is a starting point, not a guarantee.

Remember that Pip is read-only and does not move money; it’s not financial advice. Use it as a decision-support tool, not a replacement for checking your full financial picture. The category-free signal works best when you combine it with a quick glance at upcoming payments.

How Pip handles it

Pip connects to your bank accounts via a read-only, encrypted link. It does not store bank usernames or passwords, and it does not move money. Each morning, it recalculates Spendable Cash Today by analyzing your balances and upcoming obligations. You see one number, available for today, without ever building a budget.

If you have multiple accounts, Pip aggregates them and subtracts the bills you’ve taught it to expect. The result is a category-free daily signal that adapts as your money moves. Because Pip never moves money, you can check the number without fearing accidental transfers. There are no budgeting dashboards or spending trackers; just a clean interface with one number. That simple design helps you answer “Can I afford this?” in seconds, without categories. And because Pip is not financial advice, you stay in full control of your spending decisions. No guilt, no category guilt, just a number that reflects your real situation.

Before you rely on the number

Use the daily figure as a checkpoint, then pause for anything the app may not have seen yet. Look at bills due before the next payday, recent card activity that may still be pending, and transfers you already promised to savings. If one of those changed today, keep a little more cushion than the number suggests. Because Pip is not financial advice and does not move money, you stay in complete control. The daily number is a helpful starting point, not a spending cap. Pip is built to make that pause faster by keeping the view small and read-only, but the final spending decision still belongs to you.

FAQ

Do I really never need to create spending categories?

No. Pip skips categories entirely. It gives you one number that shows what’s available for today after big obligations are set aside. You decide how to spend it, no labels, no guilt.

Is this app safe for people who are nervous about connecting bank accounts?

Yes. Pip uses bank-grade encryption and a read-only connection. It does not move money. It does not store bank usernames or passwords. That design keeps your finances private while giving you a reliable daily signal.

How is Pip different from a simple balance check?

Your bank balance doesn’t subtract future bills or committed spending. Pip does, so you don’t accidentally spend rent money. The number you see is a closer picture of what’s truly available for today, no category filters needed.

Source notes

This article draws on behavioral research showing that many people abandon budgeting apps because category maintenance feels overwhelming. Pip’s category-free daily number approach is inspired by mental accounting research and cash-flow management principles. For more on why categories can fail, see budgeting is hard, Pip uses one number instead. Pip’s read-only security design is detailed on our security page.