Quick answer

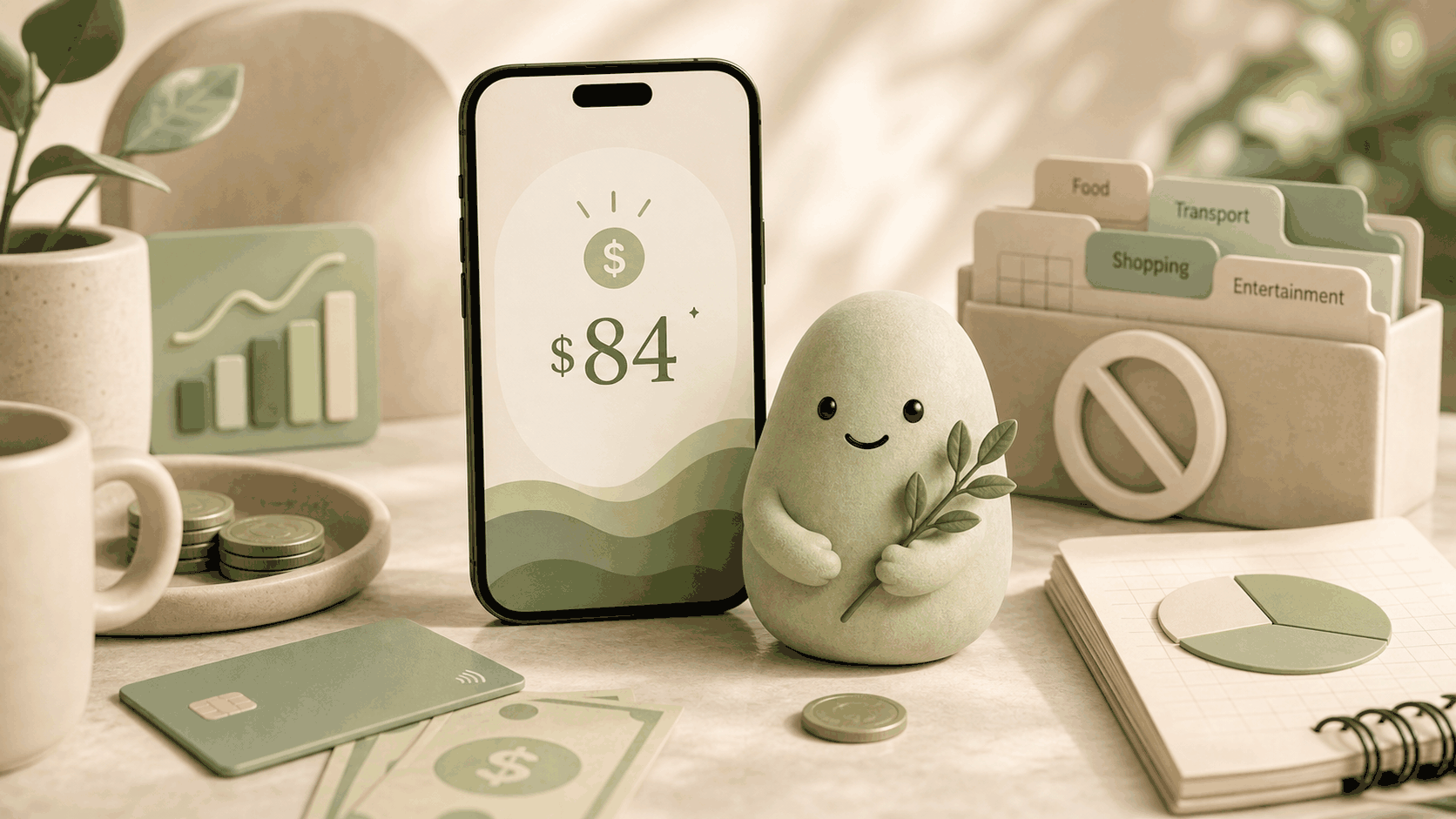

When you're about to buy, you need a number that filters out what's already spoken for, including bills, savings you want to protect, and spending you've already committed to. A raw bank balance hides those obligations. The quick check: subtract near-term bills, protected savings, and outstanding debit or card charges from your usable cash. What remains is a spendable-today estimate you can glance at before you spend. Pip does that math and gives you one number, Spendable Cash Today, so you don't have to calculate.

A realistic money example

Even though $1,200 appears in your banking app, only $450 is actually free for today once you remove what's already spoken for. That gap between a balance and an actionable number is where trouble hides. Without this step, it's easy to spend $80 on lunch and $100 on a night out, then wake up to find you've eaten into bill money. Checking a spendable-today figure before you pay helps you avoid that.

How to estimate it

Start with the money that's actually available right now: the balance inside your spending accounts (checking and any savings you treat as everyday). Then remove three categories that aren't free for today:

1. Near‑term bills: anything due before your next paycheck (rent, utilities, subscriptions, credit‑card minimums). 2. Protected savings: money you've mentally set aside for emergencies, a specific goal, or just don't want to accidentally spend. 3. Already‑committed spending: debit‑card authorizations, scheduled transfers, and recent swipes that haven't yet cleared but are already out the door.

The remaining pool is what you can reasonably consider available for today. The formula is:

Estimated spendable today = usable cash − near‑term bills − protected savings − already‐committed card/debit spending − other known obligations

You can do a rough version in your head, but it's easy to miss a bill or forget a haircut you booked yesterday. Automating the subtraction helps avoid that.

Limits

Even a careful estimate has blind spots. Delayed transactions (like a pending refund or a restaurant tip that hasn't posted) can make your balance look higher than it really is. Stale connections or a missing account (like a second checking account you forgot to link) will produce an incomplete number. Unexpected bills (a car repair, a surprise subscription renewal) aren't captured unless you manually add them. This number is not financial advice; it's just a snapshot of what the data says you can work with today, not a guarantee that every obligation has been captured. Always review large purchases against what you know.

How Pip handles it

Each day, Pip reads your linked accounts using read-only access (it does not move money) and automatically subtracts upcoming bills, without duplicates, across all your accounts. It also factors in protected savings you've marked and any committed debit spending it detects. The result is Spendable Cash Today, a single number you can glance at in seconds before a purchase.

Since Pip never stores bank usernames or passwords and works read‑only, your money stays exactly where it is. Think of it as a daily signal, not a budget and not financial advice. It won't tell you what to buy; it just shows you the amount that's available for today after obvious commitments are subtracted. That turns a stressful pre‑purchase moment into a quick, low‑pressure check.

Before you rely on the number

Treat the daily figure as a checkpoint, then pause to consider anything the app might have missed. Check bills due before the next payday, recent card activity that may still be pending, and transfers you've committed to savings. If one of those changed today, leave a little extra cushion beyond what the number shows. Pip is designed to make that pause quicker by keeping the view simple and read-only, but the final spending decision is always yours.

FAQ

Does this work if I use credit cards for everything?

Yes. Pip can include credit‑card balances and upcoming payments in its calculations, so your daily number shows what's truly available after credit obligations. Just remember: the final number is a spending signal, not a credit‑limit recommendation.

Can I use Pip to check before a big purchase?

You can, but it's most useful for everyday decisions. For a large one‑off expense, you'll still want to look at the full picture yourself. Pip gives you Spendable Cash Today as a starting point, but since it can't account for every future event, it's not a substitute for your own judgment.

What happens if an account connection breaks?

Pip can only reflect what it sees. If a bank connection gets stale or a linked account is removed, your Spendable Cash Today number becomes incomplete. Pip alerts you when connections need attention, but the number you see is always a read‑only snapshot from whatever accounts it can access.

Source notes

- Pip uses a read-only account connection, does not move money, does not store bank usernames or passwords, and is not financial advice. This article draws on Pip's product approach and the common gap between a bank balance and what's truly spendable on any given day. It was updated after Pip's public launch and reflects the current Spendable Cash Today calculation.