Quick answer

To avoid spending bill money by mistake, separate your committed cash from today's spending room. Look at your bank balance, then subtract everything that must leave your account before your next payday: rent, utilities, loan payments, subscriptions. The leftover is what you have available for groceries, gas, and everyday purchases right now. When you check that single spendable number each morning, you stop reaching for dollars that are already spoken for. This habit replaces the false confidence a raw bank balance gives you.

Why this happens

A checking account balance looks solid until a scheduled withdrawal pulls it down without warning. That number on your bank app is a snapshot of the past, not a plan for the future. It doesn't know you committed $1,200 to rent three days from now or that your car insurance auto-debits tomorrow. Without subtracting those obligations, the balance feels like free money. You swipe a debit card for lunch, top off the gas tank, and grab a coffee. Meanwhile, a bill you can't skip is about to clear. By the time the payment clears, your balance drops below what you need, leading to overdrafts or frantic transfers.

The gap between your bank balance and what you actually have shrinks once you subtract upcoming commitments. Without that step, your brain treats the full balance as permission to spend. Separating committed funds from truly spendable cash breaks that pattern and keeps surprise shortages off your screen.

How to estimate it

Start with your checking account balance right now. Then list every bill, subscription, and loan payment that will be withdrawn before your next income deposit. Subtract those fixed commitments. Next, set aside a rough amount for necessities you'll buy in that same window: groceries, fuel, and any recurring small purchases you can't skip. The dollars that remain after all subtractions are your spendable cash for today.

Think of it as a simple decision-support formula: Spendable today = usable cash - near-term bills - protected savings - already-committed card/debit spending - other known obligations. This isn't a rigid budget; it's a clarity tool. Keep your estimate simple so you'll actually check it. A pen-and-paper note on your phone, or a quick glance at a spreadsheet, can be enough to make the mental shift from "my balance says I'm fine" to "I have $X available for today."

The number can change daily because new pending transactions, payday timelines, and surprise expenses move the needle. Even a rough "bill-safe" estimate makes it harder to accidentally spend money that's tagged for a due date. You don't need to be precise to the cent. A small rounding difference won't break you. The practice of subtracting before spending is what changes your behavior. Over time, you'll spot patterns, like how many subscriptions hit mid-month, and adjust your number naturally.

For example, imagine Maya gets paid biweekly. Her checking account shows $2,400, but several bills are due before her next paycheck. Here's a quick breakdown.

After subtracting everything that's already spoken for, Maya has $360 left. That is her available for today number, not $2,400. Checking this before making any purchase helps her avoid accidentally using money that belongs to a bill.

Limits

Manual estimates break down when you forget a recurring charge or an auto-debit that hits a day earlier than expected. They also don't account for fluctuations in your credit card balance: yesterday's coffee, a last-minute gas stop, or a weekend lunch you forgot about can quietly eat into the money you thought was there. If you skip the essentials envelope, you might end up borrowing from a bill that has no grace period.

Even with careful tracking, rounding and mental math can give you a false sense of security. Surprise expenses like a parking fine, a medical copay, or a delayed paycheck can render your estimate useless overnight. A static estimate isn't the same as a number that updates with your actual transaction activity.

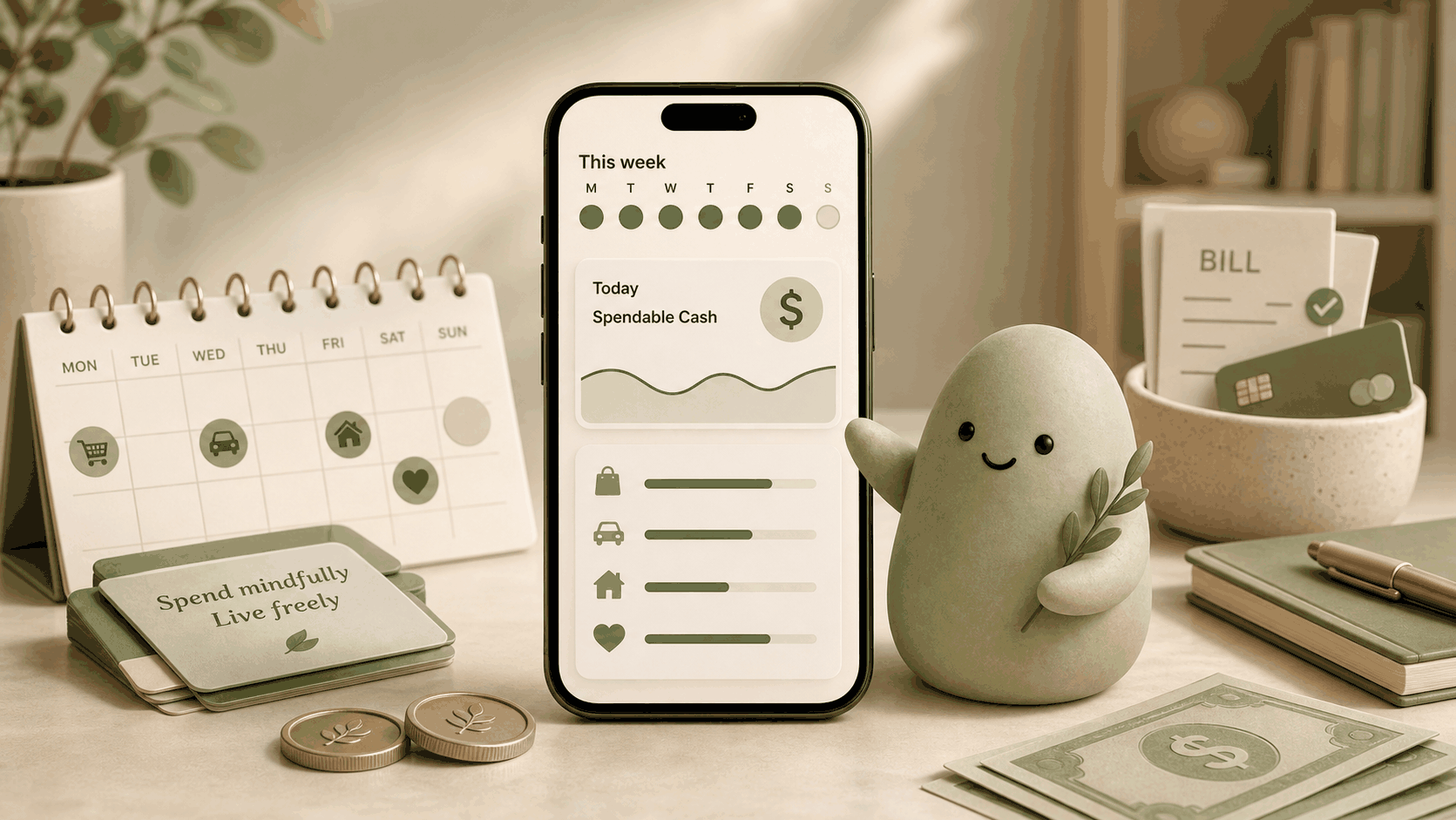

How Pip handles it

Pip connects to your checking and credit card accounts with read-only access. It does not move money and does not store your bank usernames or passwords. Instead of relying on memory, it identifies upcoming recurring debits from your transaction history, lets you add one-time bills, and subtracts credit card spending you've already committed but haven't paid off yet. The result is Spendable Cash Today, a single number that shows what's available for today without accidentally dipping into money needed for rent, utilities, or loan payments.

Pip is not financial advice. It's a decision-support tool that gives you a realistic picture of your remaining spending room. You check it before you spend, and the number already accounts for bills that are easy to miss. That's how a read-only daily signal helps you stop spending bill money by mistake.

FAQ

Why does my bank balance feel misleading when bills are due soon?

Your bank balance is a snapshot of cash right now. It doesn't account for pending automatic debits, checks you've written, or bills you've scheduled. So it's a look back, not a look ahead. By the time a payment clears, you might have already spent that cash, leaving your account short.

Can I still overspend if I estimate my spendable cash manually?

Yes. Your manual estimate depends on which bills you remember and which due dates you track. A forgotten subscription or a check that clears late can skew the number, making it easy to dip into bill money. That's why a tool that automatically spots recurring obligations tends to be more reliable than mental math.

Does Pip warn me before a bill is due?

Pip doesn't send alerts before bills are due. But its Spendable Cash Today number already subtracts upcoming recurring payments and credit card spending you've committed. When a future bill would push that number close to zero, it's a quiet signal to ease up on spending, so you rarely need an explicit alert.

Source notes

- Pip uses a read-only account connection, does not move money, does not store bank usernames or passwords, and is not financial advice. Pip's Spendable Cash Today relies on transaction data from connected accounts and user-supplied bill amounts. Missing accounts, unlinked credit cards, or delays in bank data refresh can make the estimate slightly off. Always verify critical bill dates directly with your providers. For a deeper look at how the number is calculated, see How the number works.