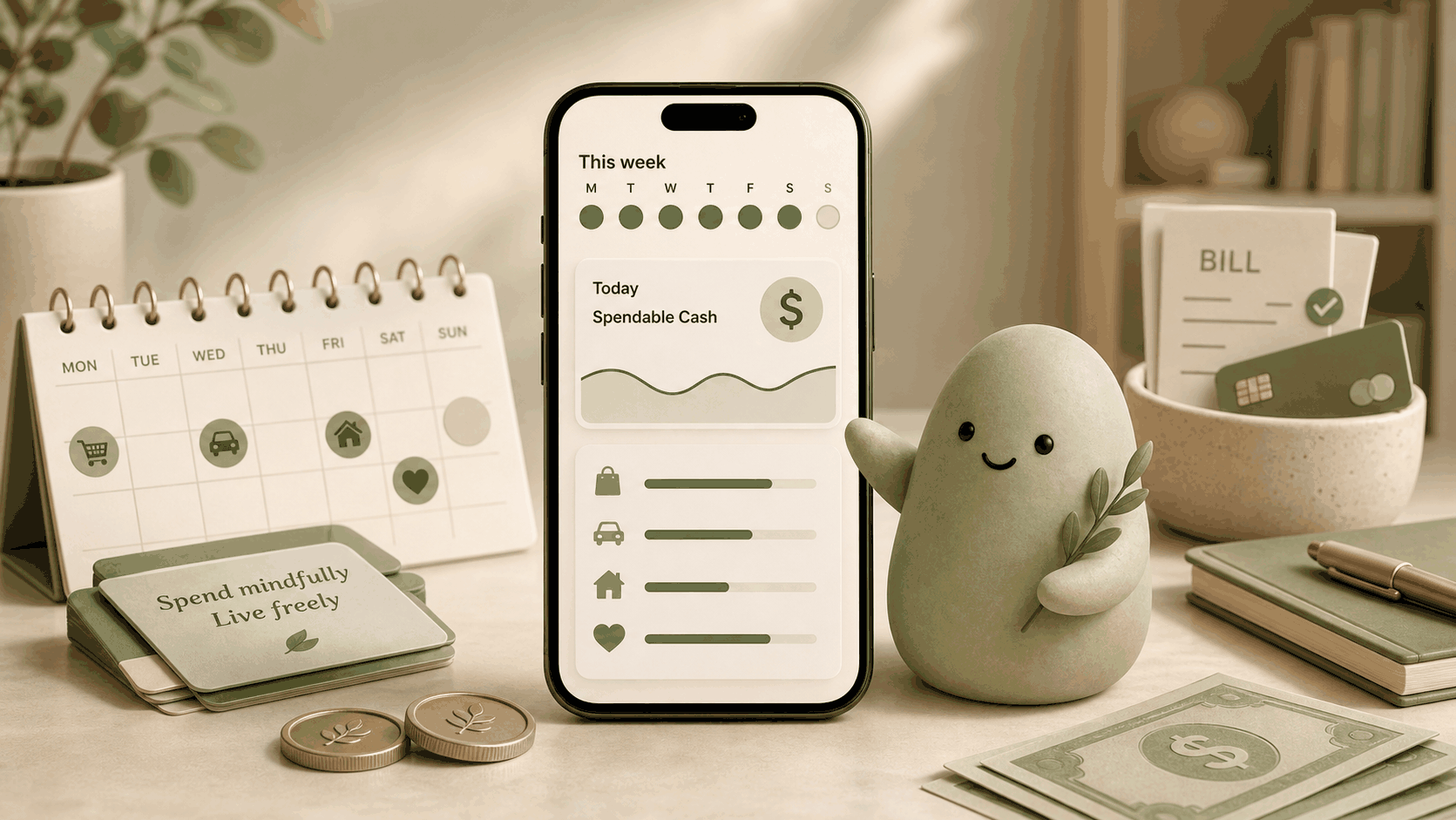

Quick answer

You can create a weekly spending plan without a traditional budget by checking one number every morning. That number already accounts for upcoming bills, savings, and the days until your next payday. Pip’s Spendable Cash Today gives you exactly that. Instead of setting category limits, you look at a single figure that tells you what’s available for today. That daily check creates a natural weekly pacing rhythm without spreadsheets or guilt.

A realistic weekly pacing example

Suppose your take-home after fixed bills is $420, and you need it to last seven days. A classic budget might assign a $60 daily limit and track categories. Without one, you can simply watch your daily available number and adjust as the week goes.

The numbers shift: a light day opens up more room later, a heavy day tightens things. You don’t set a firm allowance. Notice whether today’s figure is higher or lower than yesterday, and that awareness becomes your weekly pacing rhythm.

How to estimate it

Start with the cleared cash in your bank account. Subtract bills due before your next payday, any savings you want to protect, and card purchases that haven’t cleared yet. What’s left is your usable cash. Divide that by the days remaining until payday to get a rough daily average. Doing this by hand a couple of times a week works, but it’s tedious. Pip automates the same calculation each morning, pulling your balances and upcoming payments. It gives you a single updated number that already accounts for bills and card swipes you might overlook. The formula: usable cash minus near-term bills minus protected savings minus already-committed spending minus other obligations. Pip recalculates so you don’t have to.

What can make this estimate wrong

A weekly number can move around. A delayed check or refund can make your balance look bigger than it is; an unexpected bill can shrink it. Forgetting an account leaves gaps. Irregular income stretches your pay cycle: a longer gap between paychecks shrinks the daily number. A static Monday-morning worksheet can go stale fast, which is why a daily-refreshed number is more dependable. Pending card charges and subscriptions on odd dates also throw off a fixed estimate. Treat the number as a rolling guide, not a guarantee. Pip accounts for many moving parts, but no tool can predict every surprise.

How Pip handles it

Pip uses a read-only connection, so it can see balances and transactions but does not move money and does not store bank usernames or passwords. Each morning it pulls your latest transactions, identifies upcoming bills, and subtracts what’s needed for the rest of your pay cycle. The result is Spendable Cash Today, a number that shows what’s available for today without endangering standing orders or your savings.

Because it recalculates daily, Pip works as a low-pressure pacing tool. You get a fresh number each morning. If you spent less yesterday, today’s number rises; if you overspent, it drops. You check the number before larger purchases instead of managing categories. Pip is not financial advice. It never locks or moves money. It’s a decision-support companion that shows how much room you have right now, giving you a practical weekly rhythm without rigid categories.

FAQ

Can I really plan weekly spending without a budget?

Yes. Instead of pre-deciding category amounts, watch whether today’s number is trending up or down across the week. The number already subtracts bills and protects savings, so you focus on pacing, not categories.

How is Pip’s daily number different from a weekly allowance?

A weekly allowance is a fixed pool for seven days. Pip’s number recalculates each morning. A light Monday raises Tuesday’s figure; a bill clearing Wednesday lowers Thursday’s. It’s a dynamic signal, not a static target — more like a weather report for your week.

What if my bills aren’t spread evenly across the week?

Pip accounts for recurring bill due dates. On bill-heavy days the number is smaller; on light days it’s larger. You don’t need to mentally set aside amounts, because the number already accounts for them.

Does Pip automatically adjust for weekends or spending surges?

Yes. Daily updates mean a spend-heavy Saturday lowers Sunday’s number, which helps you correct course without rigid allowances. The week’s natural ups and downs produce the same result as a handwritten plan, with far less effort.

Source notes

This article draws on common personal finance pacing strategies that rely on a daily spending number instead of category budgets. The concepts align with ideas from behavioral economists who study decision-making under scarcity. Pip’s product design applies these principles automatically. No external research paper is cited directly; the piece is based on widely shared best practices for straightforward weekly money management.