Quick answer

A simple finance app without budgeting gives you one daily answer instead of a dashboard to maintain. Pip uses read-only account data to estimate Spendable Cash Today after upcoming bills, planned savings, and committed card spending. There are no categories, spreadsheets, or manual transaction logs. You get a quick decision-support signal for what is available for today, while Pip never moves money and is not financial advice.

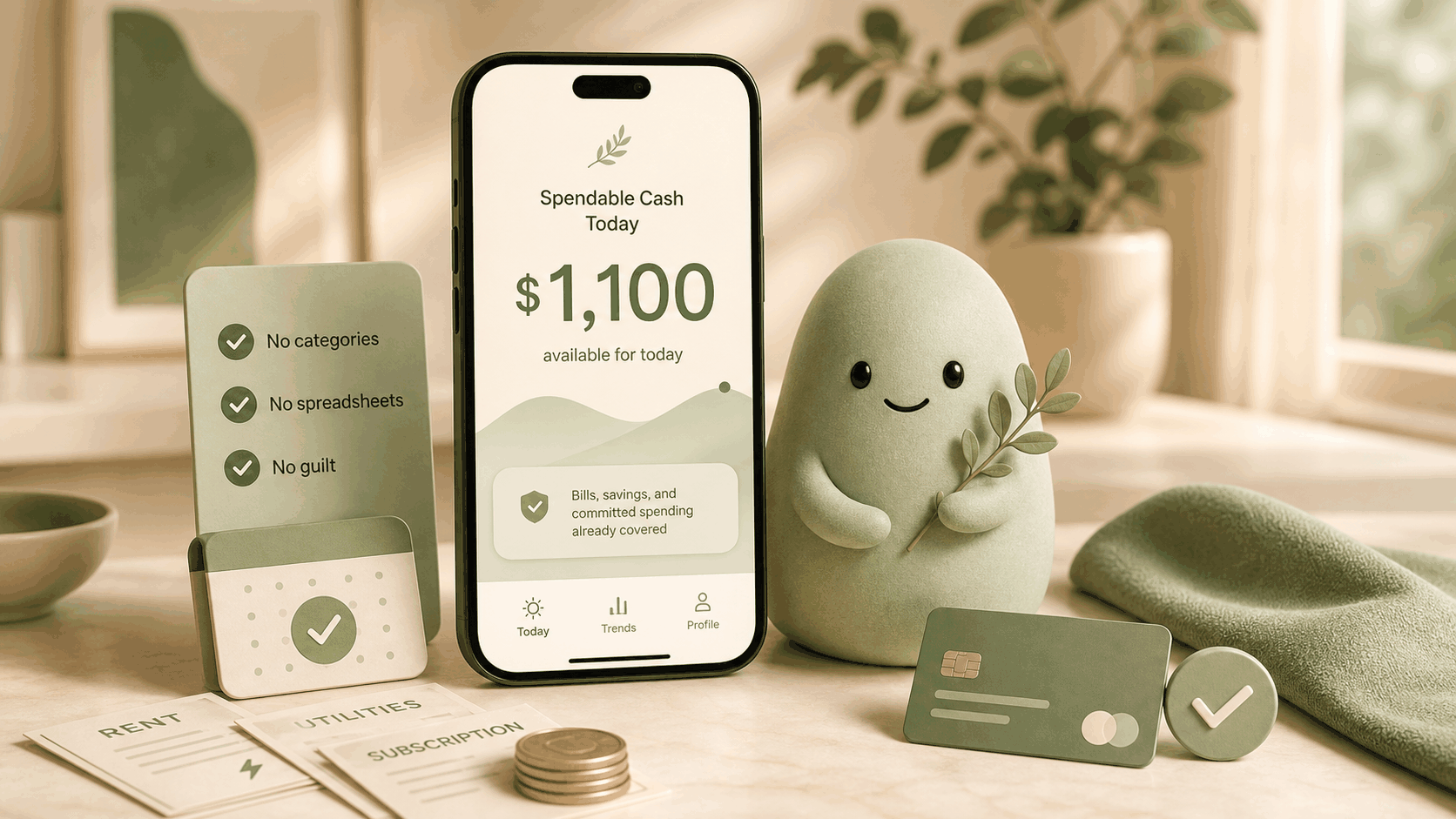

A realistic example

If your raw bank balance reads $3,200, it’s easy to feel like you have plenty of room. But after holding back the money needed for bills due soon, protecting a savings cushion, and accounting for pending card transactions you’ve already authorized, the amount actually available for today might be just $1,100. Pip surfaces that smaller, truer number every morning—so you don’t have to do the mental math yourself.

How to estimate it

You can approximate your own daily spendable amount with a simple subtraction path: start with your current usable cash across checking and any other liquid accounts. Next, subtract all bills you expect to pay within the next 10–14 days—rent, utilities, subscriptions, minimum card payments. Then subtract the amount you intend to keep as a protected savings buffer (say, a monthly savings goal set aside). Finally, subtract any card or debit spending you’ve already committed but that hasn’t cleared yet, and any other known obligations that must come out of the same cash. The formula looks like this: usable cash – near‑term bills – protected savings – already‑committed spending – other obligations = spendable today.

The biggest challenge is keeping the list of upcoming bills current and consistently remembering to hold back savings—especially when your income and expenses shift week to week. That’s why many people end up doing the math only occasionally, or skip it entirely and rely on a raw bank balance that can feel misleadingly large (see Why your bank balance is misleading). A simple finance app like Pip automates this recalculation every day so you don’t have to.

What can make this estimate wrong

Any daily spending estimate has limits. If an account isn’t connected—or the connection is stale—the number will be incomplete. Large, unexpected bills that land outside your regular cycle (a car repair, an emergency) can shift your real‑world position quickly. Pending refunds or delayed transactions might not appear in time, making your available cash look lower than it is. Income that is irregular or lumpy (freelance work, tips, quarterly dividends) isn’t automatically factored in unless you manually adjust your savings buffer.

Additionally, the estimate is only as good as the data window it considers. Pip looks at the next 14 days of known bills, so obligations beyond that horizon aren’t being subtracted yet. And like any read‑only tool, Pip cannot predict what you’ll spend—it simply surfaces what’s available after known deductions. The number is a decision‑support signal, not a guarantee, and it should never be treated as financial advice.

How Pip handles it

Pip uses a read‑only connection to your bank accounts through Plaid, a bank‑grade data partner. It does not move money, does not store your bank usernames or passwords, and cannot initiate transactions—your funds stay exactly where they are. Each morning, Pip pulls your latest balances, identifies known upcoming bills, holds your chosen monthly savings amount to the side, and subtracts already‑committed card spending. The result is one number: Spendable Cash Today, refreshed daily.

Because the calculation is read‑only and automated, there’s no data entry for you to maintain. You’re not building a budget—you’re just getting a truer picture of the money that is available for today. Pip is not financial advice; it’s a low‑friction companion that helps you make quick spending decisions without the overhead of traditional budgeting. If your financial life includes variable income or infrequent large expenses, you can adjust your savings cushion manually, giving you a signal that adapts to your reality without turning into a full budgeting chore.

FAQ

Why choose a simple finance app without budgeting instead of a full‑featured budgeting tool?

Traditional budgeting apps ask you to categorize, forecast, and track every dollar. That works well for people who enjoy that level of detail, but for everyone else it can feel like a part‑time job. A simple finance app like Pip replaces that overhead with one daily number. You get a quick check that helps you decide whether to grab that coffee or wait until tomorrow—without maintaining a single category or spreadsheet. The result is lower‑effort, lower‑guilt money awareness that fits into a busy day.

Does Pip require me to track every purchase?

No. Pip doesn’t ask you to log purchases or label transactions. It simply reads your account balances, recognizes known bills, and protects your chosen savings amount. The remaining Spendable Cash Today updates as transactions clear. You can still see where your money goes if you want to review your account, but you’re never required to manually track anything. The experience is designed for people who want an answer—not a record‑keeping exercise.

How is Pip different from just checking my bank balance?

Your bank balance shows the raw total in your account, but it doesn’t tell you what that money is already earmarked for. Rent, upcoming subscriptions, and the savings you promised yourself all look like “available” cash until you mentally subtract them—which most of us forget to do. Pip does that subtraction for you and shows the smaller, more realistic number that’s truly available for today. (Read more: Why your bank balance is misleading.)

What if my income is unpredictable?

Pip works even when income isn’t a steady paycheck. The daily number is based on the cash you actually have, not on a predicted future deposit. If you’re a freelancer or you work tipped shifts, you can still see what’s safe to use right now by adjusting your savings cushion when a big deposit lands. That gives you a decision‑support signal that reflects your real‑time position without requiring a traditional budget template.

Source notes

- Pip uses a read-only account connection, does not move money, does not store bank usernames or passwords, and is not financial advice. The daily spendable formula used here—bringing together usable cash, near‑term bills, protected savings, and committed spending—is the same logic behind Pip’s Spendable Cash Today model. Pip obtains bank data through Plaid’s read‑only API and does not store login credentials. Last reviewed based on Pip’s current approach (May 2025).