Quick answer

Overspending before payday often stems from one mistake: checking your bank balance and assuming that money is yours. Your real spending room is much smaller after accounting for upcoming bills, savings, and what you’ve already committed this month. The solution is to swap the bank balance for a daily spendable number, a figure that subtracts those obligations before you spend. Focus on that single number each morning, and you spend less, stopping the paycheck-to-paycheck panic.

A realistic example

Imagine you check your bank app on a Monday morning. The balance says $2,200. It feels safe. But between now and Friday, you’ve promised $800 to rent and credit cards, you want to keep $300 completely off‑limits for your savings goal, and you already tapped your debit card for $250 worth of groceries and gas. You’d be spending money that isn’t actually there. When you subtract those commitments, your daily spending room shrinks dramatically:

Only $850 remains to cover everything else: coffee, a lunch out, a small impulse, all while keeping your bills and savings untouched. Without that filter, you might see the full $2,200 as spendable and overshoot by $1,350 before payday.

How to estimate it

The formula is simple in concept: Estimated spendable today = usable cash − near‑term bills − protected savings − already‑committed card/debit spending − other known obligations.

Start with your usable cash: the actual available balance in your checking account, but only the part you’re willing to spend this month. (Many people keep a minimum buffer that shouldn’t be touched.) Subtract any bill that hits before your next payday: rent, utilities, loan payments, subscriptions. Then carve out protected savings, a non‑negotiable monthly amount you’ve set aside for an emergency fund or a bigger goal. Next, subtract money you’ve already committed on a debit or credit card this month that hasn’t cleared yet; those pending charges represent tomorrow’s drain. Finally, subtract any known irregular obligations like a doctor’s visit copay or a school trip fee. The leftover is your spendable today. Adjust for the days remaining until payday to get a daily allowance, or use a tool that does the math for you. This approach shows that your bank balance is layered with promises, not free cash.

What can make this estimate wrong

No estimate is perfect. Common blind spots include forgetting irregular bills (like an annual insurance premium or a car registration), underestimating variable expenses (like a higher‑than‑usual electric bill), or ignoring pending credit card payments that haven’t yet deducted from your bank. Refunds that haven’t posted can also give a false cushion. If you connect fewer accounts than you actually use, the calculation misses money sitting in a secondary checking or savings account that could be spent. Similarly, a sudden emergency, like a car repair or a medical copay, can throw off any plan. Missing accounts, stale connections, delayed transactions, refunds, and unexpected bills can make estimates incomplete. Estimates also break down if you guess your savings amount instead of protecting it realistically. The more you automate the tracking and the more accounts you include, the closer you’ll get to a trustworthy number.

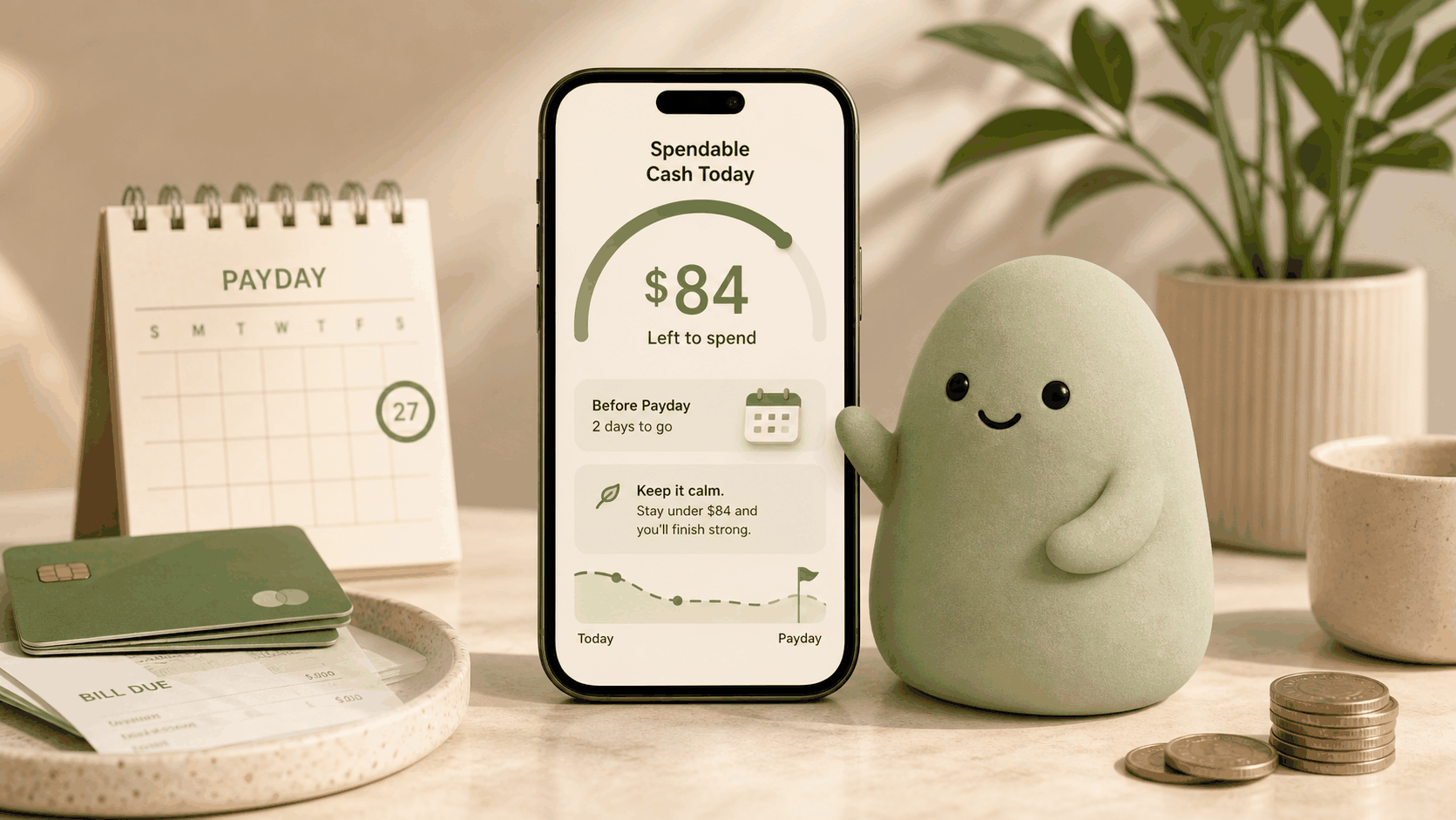

How Pip handles it

Pip connects to your checking and credit accounts through a read‑only connection. It can see transactions and balances but does not move money and does not store bank usernames or passwords. Every morning, Pip scans your upcoming bills, protected savings, and recent card activity to compute a single Spendable Cash Today number. That number replaces guesswork with a hard‑check before you spend.

The app respects your real financial boundaries. It doesn’t try to be a full‑blown budget or investment coach; it simply answers the question “How much can I safely spend right now?” By doing the subtraction work for you every day, Pip helps you internalize the true cost of your spending decisions without nagging. Over time, that awareness reins in overspending before payday, without any need for willpower. And because the connection is read‑only, there’s zero risk of accidental transfers or compromised credentials. Pip is not financial advice; it’s decision‑support software that keeps you in control.

FAQ

Why do I overspend even when my bank balance looks healthy?

Your bank balance mixes money already promised to bills, savings, and past spending with truly free cash. That big number gives a false sense of security. By focusing on a daily spendable figure, like Pip’s Spendable Cash Today, you see the real limit. Once you treat only a smaller portion as available for today, overspending becomes less likely.

Can a single daily number really help me stop overspending?

Yes, because it eliminates the mental math. Without it, every swipe feels like a gamble. Pip recalculates your number each morning, so you don’t need to remember every bill due date. A quick glance tells you if a purchase is safe. That pause alone can break the overspending cycle.

Do I need to track every purchase or build a budget?

No. Pip connects to your accounts through a read‑only connection and works behind the scenes. You don’t log receipts or set up categories. It gives you one number, no maintenance required. For people allergic to spreadsheets, that’s the whole draw.

What does $0 today mean?

It means obligations and protected savings have used up your available cash until next payday. It’s not a punishment; it’s a warning light. You can still spend in an emergency, but seeing that zero encourages you to pause and consider if the purchase is essential.

Source notes

- Pip uses a read-only account connection, does not move money, does not store bank usernames or passwords, and is not financial advice. The estimation method described here relies on the mental‑accounting concept that people treat money differently depending on its label (Thaler, 1999). Pip’s Spendable Cash Today applies that concept by automatically subtracting labeled commitments. This article is for educational purposes and is not financial advice. Regular account review and professional guidance are recommended for complex situations.